Fleet Intelligence · EV Financing

NBFCs do not just finance vehicles. They finance moving assets whose value, location, battery health, and recovery risk change every single day. Telematics gives them the visibility they need after loan disbursement.

June 2026 · 20 min read

India’s electric vehicle revolution is no longer a future forecast. It is unfolding right now. In FY2025–26, EV sales in India crossed approximately 24.5 lakh units, a 24.6% year on year jump, with overall EV penetration reaching roughly 8.5% of all vehicle registrations [1]. The Indian EV market, valued at USD 5.28 billion in 2025, is projected to surge past USD 17 billion by 2032, growing at a CAGR of 19% [2]. Battery electric passenger vehicle sales alone hit a record 1,76,500 units in calendar year 2025, registering a 77% year on year growth [3].

For Non-Banking Financial Companies (NBFCs), this rapid electrification creates both a massive lending opportunity and a fundamentally new category of asset risk. According to a credit ratings agency, NBFC vehicle loan AUM is set to reach approximately ₹11 lakh crore by March 2027, growing at a steady 16 to 17% annually [4]. The India EV financing market alone is estimated at USD 3.59 billion in 2026 and is projected to reach USD 28.79 billion by 2031, growing at a staggering 51.62% CAGR [5]. NBFCs, along with fintech lenders, are carrying the bulk of this EV financing load, particularly in segments and geographies where traditional banks remain cautious.

Yet the asset they are financing is fundamentally different from an Internal Combustion Engine (ICE) vehicle. An EV’s battery pack accounts for 30 to 50% of the total vehicle cost [6]. That battery degrades based on charging habits, temperature exposure, and usage patterns, factors that are entirely invisible to a lender relying on traditional paperwork and periodic check ins. A financed EV may look physically intact while its battery health is quietly declining, eroding resale value and recovery potential without the NBFC ever knowing.

This article explores a critical question: once an EV loan is disbursed, how does an NBFC maintain visibility into a moving, depreciating, battery dependent asset? The answer lies in advanced telematics, specifically in the combination of live location intelligence, geofencing, battery health monitoring, usage analytics, and early warning systems that transform post disbursement risk management from guesswork into a data driven discipline.

The Scale of the Opportunity and Risk

India’s EV financing market is projected to grow from USD 2.37 billion in 2025 to USD 28.79 billion by 2031 at a 51.62% CAGR [5]. NBFC vehicle loan AUM is on track to hit ₹11 lakh crore by March 2027 [4]. With the NBFC sector’s GNPA ratio at 3.4% [7] and EV lending growing faster than any other vehicle segment, the quality of post disbursement asset monitoring will directly determine whether this growth remains profitable.

The Post Disbursement Blind Spot: Why EV Financing Demands Continuous Asset Visibility

Traditional vehicle finance models are built around a snapshot assessment. The NBFC evaluates the borrower’s creditworthiness, income stability, repayment capacity, and the vehicle’s on road value at the time of loan origination. Once the loan is disbursed and the vehicle leaves the dealership, visibility drops sharply. The lender relies on EMI collection patterns and occasional manual check ins to gauge asset health.

For ICE vehicles, this approach worked reasonably well because the vehicle’s value depreciation was relatively predictable, resale markets were well established, and the mechanical condition of the engine did not fluctuate based on daily usage habits. EVs change this equation completely.

Consider what an NBFC typically does not know after disbursing an EV loan:

Where the vehicle actually operates. A borrower may declare a home city and intended usage zone during the loan application. But the vehicle could be operating across state lines, in a different city entirely, or even in conditions (high altitude, extreme heat, rough terrain) that accelerate wear. Without live location data, the lender has no way to verify this.

How the vehicle is being used. A loan approved for personal commuting may be underwriting a vehicle that is actually running 150+ kilometres daily as an unlicensed commercial cab. This level of overuse accelerates battery degradation, tyre wear, and suspension damage, all of which erode the asset’s residual value well before the loan tenure ends.

Whether the battery is holding its value. The battery is the single most expensive component of an EV. In India, replacement costs range from ₹1.5 lakh to ₹12 lakh depending on the vehicle, which amounts to 30 to 50% of the original vehicle price [6][8]. An EV that is physically present and operational may have a battery at 65% State of Health (SoH), making it worth significantly less than the outstanding loan amount. Without battery telemetry, this value erosion is invisible to the lender until recovery becomes necessary, at which point the shortfall becomes a write off.

Whether the asset is at risk of disappearance. Vehicle inactivity, device tampering, cross border movement, or prolonged parking at unknown locations are all precursors to asset hiding or loss. Traditional check ins detect these signals weeks or months too late.

This post disbursement blind spot is not a minor inconvenience. It is a structural risk that grows with every EV loan in the portfolio. As EV penetration climbs toward the projected 9.5 to 10% in FY2026–27 [1], and as NBFCs expand their EV books to capture this growth, the cost of not seeing what happens to the asset after disbursement becomes unacceptably high.

Live Location Intelligence: The Foundation of Asset Monitoring

At the most fundamental level, an NBFC financing an EV needs to know where the asset is. Not once a month. Not when the borrower self reports. In real time, with historical context.

Modern telematics systems provide this through a continuous stream of GPS data that gives lenders several critical capabilities. Live GPS location delivers the vehicle’s current position, updated at frequent intervals, providing an accurate and persistent picture of the asset’s whereabouts. Last known location ensures that even if a device temporarily loses connectivity due to network gaps, underground parking, or remote areas, the system retains the most recent reported position, giving recovery teams a starting point rather than a blank slate.

Trip history and route playback go beyond current position. They create a complete historical record of every journey the vehicle has taken, including routes, distances, speeds, stops, and durations. For an NBFC, this data is a behavioural fingerprint. It reveals whether a vehicle financed for urban commuting is actually running long distance routes. It shows whether a vehicle that was supposed to be in Mumbai is spending most of its time in another state. It surfaces patterns like unusual night movement or extended parking at unknown locations.

Movement status and parked duration provide instantaneous information on whether the vehicle is moving, idling, or stationary. Prolonged inactivity at an unfamiliar location, for instance, can be an early signal of abandonment or an attempt to hide the asset from recovery teams.

The business benefit is direct and measurable: when repayment issues surface, the lender is not starting from zero. The asset’s last known location, its recent movement trajectory, and its typical operational pattern are already documented. This reduces the initial discovery phase of recovery, which in traditional vehicle finance can take days or even weeks of manual fieldwork, to a matter of minutes.

Several NBFCs in India are already recognising this. One of the largest vehicle financiers in the country has been deploying telematics based tracking for its financed portfolio to enhance early warning systems and improve collection outcomes [9]. As the industry matures, live location intelligence is moving from a “nice to have” to a baseline requirement for any serious EV lending operation.

Geofencing: Turning Passive Monitoring Into Active Risk Detection

Live location tells you where the asset is right now. Geofencing tells you when the asset goes somewhere it should not.

A geofence is a virtual geographical boundary that an NBFC defines around approved operating zones, restricted areas, or high risk locations. When a financed EV enters or exits these zones, the telematics system triggers an automatic alert, notifying the lender without any manual intervention. This transforms location monitoring from a passive data feed into an active early warning system.

The practical applications for NBFCs are numerous and immediately actionable. Approved operating zone enforcement allows lenders to set boundaries around the city or state where the borrower declared the vehicle would operate. If a vehicle financed in Pune is suddenly operating consistently in a different state, the lender receives an alert and can engage the borrower to understand the situation before it escalates.

Border proximity alerts notify lenders when a vehicle approaches state or national borders. For commercial EVs, particularly electric three wheelers and light commercial vehicles that form a significant chunk of EV financing in India, cross border movement can indicate asset diversion or an attempt to move the vehicle beyond the lender’s operational recovery reach.

Unusual stoppage detection identifies when a vehicle parks at an unknown or suspicious location for an extended period. This is particularly valuable because asset hiding often begins with the vehicle being moved to a new location and kept stationary there while the borrower negotiates or delays repayment.

Route deviation monitoring, especially for commercially financed EVs, flags when vehicles consistently deviate from expected operational routes. If a fleet of electric delivery vans financed for last mile logistics starts showing irregular routes and nighttime movement, it may indicate unauthorised commercial use, subletting, or other forms of asset misuse that increase the lender’s risk exposure.

The key benefit of geofencing is timing. Traditional risk detection in vehicle finance is reactive: the lender discovers a problem after a missed EMI or a failed collection attempt. Geofencing shifts this to proactive detection, surfacing behavioural anomalies days or weeks before they manifest as financial defaults. This early detection window is where the most effective interventions happen, a simple phone call to the borrower clarifying a geofence breach can often resolve a situation that would otherwise spiral into a recovery scenario.

Immobilization: Responsible Asset Protection for High Risk Cases

In a small but critical subset of cases, when default risk is severe, when unauthorised movement is detected, or when recovery has been initiated, the ability to remotely immobilize a financed vehicle becomes a necessary tool in the NBFC’s risk management arsenal.

It is important to frame this correctly. Immobilization is not a first line response. It is not a tool for pressuring borrowers into repayment. It is a last resort capability, used only through authorised workflows, with proper safety checks, and only when the vehicle is confirmed to be stationary and in a safe condition. Responsible implementation means the vehicle can never be immobilized while in motion, ensuring no safety hazard is created for the driver, passengers, or other road users.

When implemented within this framework, immobilization offers significant benefits to NBFCs. It prevents further unauthorised movement of the asset after a recovery decision has been made. Without immobilization, a borrower who becomes aware of an impending recovery attempt can simply drive the vehicle to a new location, restarting the entire search process. Immobilization removes this possibility by securing the vehicle in place until the recovery team arrives.

It also supports faster recovery operations. A vehicle that is both located via GPS and secured via immobilization can be recovered in a single coordinated action, rather than through multiple failed attempts. This reduces the operational cost of recovery and minimises the time the asset spends in limbo.

For high value EV assets, where a single vehicle may represent a loan of ₹10 lakh to ₹25 lakh or more, the financial protection offered by responsible immobilization is substantial. It gives lenders a stronger degree of control over their financed assets, reducing the risk of total asset loss, the worst case scenario in any vehicle financing operation.

Battery Intelligence: The Risk Factor That Traditional Lenders Cannot See

This is where EV loan risk management diverges most sharply from traditional vehicle finance, and where advanced telematics platforms like Navionyx create the most differentiated value for NBFCs.

In an ICE vehicle, the engine is a durable mechanical system. It degrades, but slowly and predictably. A well maintained petrol or diesel engine can run for 2,00,000 to 3,00,000 kilometres with routine servicing. Its condition at any point is roughly proportional to its age and mileage. For an NBFC, this makes residual value estimation relatively straightforward.

An EV battery is a completely different asset. Its health is not simply a function of age and mileage. It is determined by a complex interplay of charging behaviour, temperature exposure, depth of discharge, cycle count, and cell level balance. Two identical EVs purchased on the same day and driven the same number of kilometres can have dramatically different battery health if one was regularly fast charged in extreme heat while the other was charged slowly in moderate temperatures.

The Battery Value Equation

Global lithium ion battery pack prices dropped to a record low of $108 per kWh in 2025, an 8% decline from 2024 [10]. In India, replacement costs range from ₹15,000 to ₹25,000 per kWh at the pack level, putting total replacement costs at ₹3 lakh to ₹12 lakh depending on the vehicle [6][8]. For an NBFC, a battery at 65% SoH means the asset’s recovery value could be 30 to 40% less than the outstanding loan, a gap that traditional underwriting models do not account for.

For NBFCs, this matters enormously because the battery is where most of the vehicle’s value resides. When a lender needs to recover and resell a financed EV, the resale price is primarily determined by the battery’s remaining capacity. A vehicle with a battery at 90% SoH will sell for a very different price than one at 70% SoH, even if both look identical from the outside.

Advanced telematics platforms provide NBFCs with the granular battery data they need to understand true asset quality throughout the loan tenure. This includes:

State of Charge (SoC) indicates the current charge level and operational readiness of the battery. While SoC alone does not reveal long term health, persistent patterns of deep discharge (running the battery below 10 to 15%) are damaging to long term battery life and signal misuse or operational stress.

State of Health (SoH) is the critical metric. It reflects the battery’s overall condition relative to its original capacity, typically expressed as a percentage. A battery at 80% SoH has lost 20% of its original capacity. Most OEM warranties guarantee 70 to 75% SoH over 8 years or 1,60,000 kilometres [8]. For a lender, SoH is the clearest indicator of how much the battery (and therefore the vehicle) is actually worth at any given point in the loan tenure.

Cycle count tracks the cumulative number of full charge discharge cycles the battery has undergone. Higher cycle counts correlate with greater wear. For an NBFC monitoring a portfolio of financed EVs, cycle count data helps identify vehicles that are being used more intensively than expected, which may warrant adjusted risk classifications.

Battery temperature monitoring is especially critical in India’s climate. Operating temperatures above 40°C accelerate chemical degradation within battery cells. Vehicles operating in regions like Rajasthan, Gujarat, or the Deccan plateau during summer months face measurably higher degradation rates. Telematics data that shows sustained high temperature operation alerts the lender that this particular asset may depreciate faster than portfolio averages.

Charging behaviour analysis provides insights into whether the borrower is following optimal practices. Frequent reliance on DC fast charging, consistent deep discharges below 20%, or leaving the battery at 100% for extended periods are all behaviours that accelerate degradation. Telematics data captures these patterns, enabling lenders to identify high risk charging behaviour before it translates into significant capacity loss.

Cell imbalance detection monitors voltage and capacity discrepancies between individual cells within the battery pack. Cell imbalance is often one of the earliest indicators of impending battery failure. Detecting it early through telematics gives the lender advance warning, potentially months before the battery shows visible performance degradation.

The strategic implication for NBFCs is significant. Battery intelligence transforms the EV from an opaque asset into a transparent one. Instead of discovering at the point of recovery that the battery is degraded and the vehicle is worth far less than the outstanding loan, the lender can track battery health continuously and take action early, whether that means engaging the borrower about charging practices, adjusting risk classifications, or initiating recovery before the asset loses further value.

Route and Usage Analytics: Identifying Misuse Before It Becomes a Problem

Knowing where an EV is and how healthy its battery is still leaves one critical blind spot: how the vehicle is actually being used. Usage patterns directly impact asset wear, battery degradation rate, and residual value. Telematics platforms that capture detailed route and usage data give NBFCs the ability to identify risky operational patterns early, often well before they show up in financial metrics.

Excessive daily running is one of the most common indicators of misuse in financed vehicles. If a vehicle financed for personal use is consistently logging 100+ kilometres per day, it may be operating as an unlicensed commercial vehicle. This level of usage accelerates battery cycle count, tyre wear, and overall depreciation far beyond what the loan’s risk model accounted for. Telematics data makes this immediately visible through daily distance reports.

Conversely, very low usage after disbursement is also a risk signal. If a newly financed EV shows minimal movement in the weeks following disbursement, it could indicate that the vehicle was purchased for purposes other than its declared use, possibly as collateral for an informal credit arrangement, or that the borrower is already facing operational difficulties that will soon affect repayment.

Night movement patterns, particularly in commercial EVs, can indicate unauthorised secondary use. A delivery vehicle that was financed for daytime last mile logistics but consistently operates between 10 PM and 4 AM may be subletting the vehicle for unauthorised night shift operations, increasing wear without the lender’s knowledge or consent.

Route deviation from expected business corridors, unusual stoppages at unfamiliar locations, and inconsistent operational patterns all contribute to a behavioural risk profile that telematics makes visible. For NBFCs managing portfolios of hundreds or thousands of financed EVs, this data, when aggregated and analysed, becomes a powerful tool for portfolio level risk scoring, allowing the lending team to focus attention and resources on the accounts that need it most.

Early Warning Alerts: Shifting from Reactive Recovery to Proactive Prevention

The most expensive mistake in vehicle finance is treating telematics as a recovery tool. Recovery, by definition, happens after a loan has already gone bad. The true value of telematics for NBFCs lies upstream: in the early warning signals it generates before default occurs.

A well configured telematics system continuously monitors multiple data points and flags anomalies that, based on industry patterns and historical data, correlate with increased default risk. These signals, individually, may not confirm a problem. But in combination, they form a risk picture that gives lenders a critical intervention window.

Vehicle inactivity beyond expected thresholds: A commercial EV that goes inactive for 5 or more consecutive days, particularly in segments like electric three wheelers or last mile delivery vehicles where daily operation is the norm, is a strong leading indicator of operational distress. The borrower may be facing route loss, mechanical issues, or personal circumstances that will soon affect repayment.

GPS device disconnection or tampering: When the telematics device is tampered with, disconnected, or shows persistent power cut alerts, it is one of the most serious red flags available to a lender. In the vast majority of cases, device tampering is an intentional act by a borrower who is preparing to hide the asset. This signal, when acted on immediately, can prevent a routine collection issue from becoming a full recovery operation.

Rapid battery health decline: A sudden or accelerating drop in SoH, abnormal temperature spikes, or repeated deep discharge events indicate either severe misuse or an underlying battery defect. Either way, the asset is losing value faster than projected, and the lender’s risk exposure is increasing in real time.

Repeated geofence breaches: Occasional geofence exits may have legitimate explanations (a family trip, a delivery to a new area). But consistent, repeated breaches of approved operating zones signal a borrower who is either disregarding loan terms or has changed the vehicle’s operating profile without informing the lender.

Changes in charging behaviour: A borrower who previously charged regularly and maintained healthy SoC levels but suddenly shifts to erratic, infrequent charging or consistent deep discharges may be experiencing financial stress (unable to afford regular charging) or operational changes that affect the asset’s health.

The power of these signals is not in any single alert. It is in the pattern. A telematics system that can aggregate these data points across the portfolio and assign risk scores to individual accounts gives the NBFC’s collections team a prioritised list of accounts that need proactive engagement. A phone call, a field visit, or a restructured repayment plan at this stage can often resolve an emerging problem and preserve both the loan and the customer relationship.

This shift from reactive recovery to proactive prevention is, in our experience at Navionyx, the single most impactful outcome of deploying telematics for vehicle finance. It does not eliminate defaults entirely. But it significantly reduces the number of accounts that progress from early stress to full default, and it dramatically improves recovery outcomes for those that do.

Asset Recovery: Faster, Smarter, and Data Driven

Despite the best proactive measures, a percentage of loans will inevitably turn non performing. When this happens, the speed and efficiency of asset recovery directly impacts the NBFC’s financial outcome. Every day a defaulted vehicle remains unrecovered is a day of additional depreciation, a day of potential further battery degradation, and a day of increased total loss risk.

Telematics transforms the recovery process from a manual, often frustrating operation into a streamlined, intelligence led effort. For a comprehensive look at the legal and operational framework for EV asset recovery, see our detailed guide on EV loan asset protection for NBFCs.

When a loan is classified for recovery, the telematics system immediately provides the recovery team with the vehicle’s last known location, its recent movement history over the past days and weeks, route playback showing common parking spots and frequent destinations, a log of any geofence breaches or device tampering attempts, and current vehicle status (moving, parked, or inactive). This intelligence package means the recovery team can plan a single, well coordinated retrieval action rather than conducting multiple speculative visits to addresses that may be outdated.

For EV specific recovery, battery health data adds another critical dimension. Before dispatching a recovery team, the NBFC can assess the battery’s SoH to estimate the likely resale value of the recovered asset. This informs whether a full recovery operation is financially justified, or whether a negotiated settlement might be more cost effective. This level of decision making precision is simply not available without telematics data.

Telematics records also serve as documented evidence of vehicle usage patterns, which can be valuable in legal proceedings or disputes. If a borrower claims the vehicle was not in their possession or was being used differently than what the data shows, the telematics record provides an objective, timestamped account that supports the lender’s position.

The Bigger Picture: Telematics as an Underwriting Intelligence Layer

Everything discussed so far focuses on post disbursement risk management: monitoring, alerting, and recovering after the loan has been given. But the data generated by telematics also feeds back into the underwriting process itself, creating a virtuous cycle of improving risk assessment over time.

As an NBFC accumulates telematics data across hundreds or thousands of financed EVs, patterns emerge that refine future lending decisions. The lender begins to understand which vehicle models show faster battery degradation in specific Indian climatic zones, which borrower usage profiles correlate with higher default rates, which geographic corridors produce more geofence breaches and recovery challenges, and how charging infrastructure availability in a borrower’s area affects vehicle usage and battery health.

This data is, in essence, a proprietary risk intelligence asset. It allows the NBFC to price risk more accurately, set loan to value ratios that reflect real world depreciation curves rather than assumptions, and identify high risk loan applications before disbursement rather than after default.

In a market where EV financing is growing at over 50% CAGR [5] and residual value benchmarks for EVs are still being established, the NBFC that builds this data advantage earliest will have a significant competitive edge. It will be able to lend more confidently, at better rates, and with lower loss ratios than competitors who are still underwriting EVs with ICE era models.

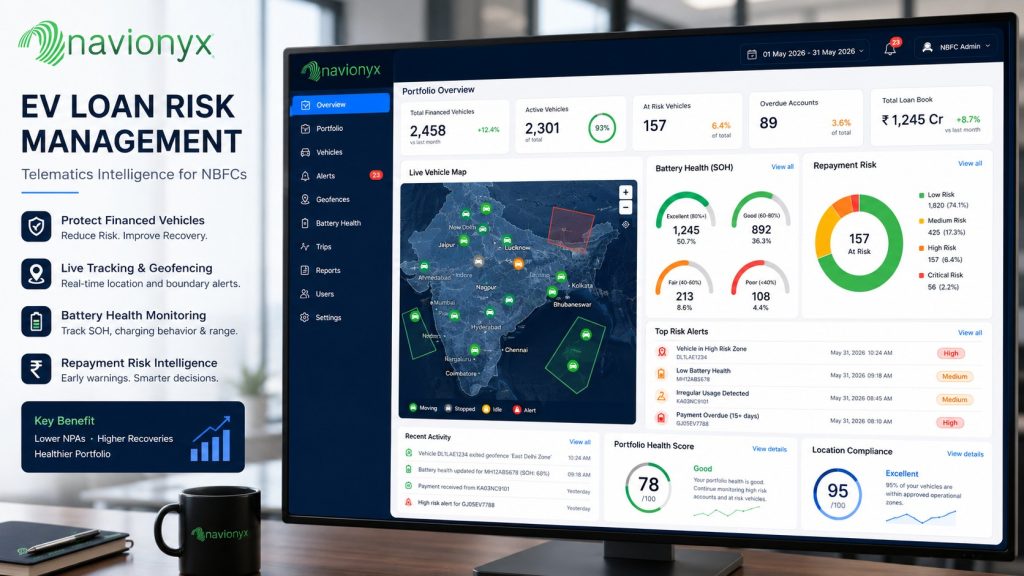

How Navionyx Helps NBFCs

Navionyx understands these challenges because we work with lenders and fleet operators who face them every day. Our telematics platform is specifically designed to give NBFCs the complete visibility they need across the entire loan lifecycle. This includes live vehicle tracking with precise, real time GPS location for every financed EV, accessible through an intuitive lender dashboard. Detailed trip history and route playback allow loan monitoring teams to analyse past movements, verify usage patterns, and support recovery planning with historical data.

Our advanced geofencing capabilities enable NBFCs to create customisable virtual boundaries for approved operating zones, restricted areas, and border proximity alerts, with instant notifications when boundaries are breached. For high risk cases, immobilization relay support provides secure, responsible remote immobilization, designed to operate only when the vehicle is stationary and following authorised workflows.

Comprehensive EV battery analytics, covering SoC, SoH, temperature, cycle count, charging behaviour, and cell imbalance, give lenders continuous visibility into the most valuable and vulnerable component of the financed asset. Proactive alerts for misuse and abnormal activity are automatically triggered by deviations from normal usage patterns, battery degradation events, or device tampering, giving collections teams early warning signals that enable intervention before default.

A dedicated lender dashboard provides a centralised view of the entire financed EV portfolio, with customisable reports, risk scoring, and analytics that support both operational decision making and strategic portfolio management. For NBFCs with existing loan management systems, seamless API integration enables automated data flow between the telematics platform and the LMS, reducing manual effort and ensuring that telematics intelligence is embedded directly into the lending workflow.

Conclusion: Telematics Is Not a Tracking Tool. It Is an Asset Protection Layer.

The transition to EV financing represents one of the most significant shifts in the Indian lending landscape. The market is growing at extraordinary rates, with EV sales crossing 24.5 lakh units in FY2025–26, EV financing projected to reach nearly USD 29 billion by 2031, and NBFC vehicle loan AUM racing toward ₹11 lakh crore. The opportunity is undeniable.

But the asset is fundamentally different. An EV is a battery dependent, location variable, usage sensitive asset whose value changes daily based on factors that are invisible to traditional lending models. The battery alone represents 30 to 50% of the vehicle’s value, and its health is determined by operational and environmental factors that no amount of paperwork can capture.

For NBFCs, the question is not whether to finance EVs. That decision has already been made by the market. The question is whether to finance them with visibility or without it. Telematics provides that visibility: real time location, proactive geofencing, responsible immobilization, granular battery intelligence, usage analytics, and early warning systems that together form a comprehensive asset protection layer.

The NBFCs that deploy this layer will grow their EV portfolios with confidence, manage risk proactively rather than reactively, protect asset value throughout the loan tenure, and achieve better recovery outcomes when necessary. The NBFCs that do not will be lending into the fastest growing vehicle segment in India with a post disbursement blind spot that grows larger with every loan.

The choice is clear. The technology exists. The data is available. What remains is the decision to use it.

Ready to protect your financed EV portfolio?

Discover how Navionyx helps NBFCs reduce loan risk with live tracking, battery health analytics, geofencing, and asset recovery intelligence.

Talk to Navionyx →This article was researched and written with AI assistance and reviewed by the Navionyx team. Data points are sourced from publicly available industry reports and are cited below.

Sources

- an EV research firm, “India’s EV Penetration Reached 8.5% in FY2025–26,” April 2026

- a market research firm, “India Electric Vehicle (EV) Market Size, Share & Trends [2032],” June 2026

- an automotive publication, “Electric Car Sales Cross 176,500 Units In 2025: Show Blistering Growth Of Over 77%,” January 2026

- a credit ratings agency, “NBFC Vehicle Loans to Ride to ₹11 Lakh Crore by March 2027,” December 2025

- a market research firm, “India Electric Vehicle Financing Market Size & Share,” January 2026

- a used EV buying guide, “The Hidden Reality of EV Battery Replacement Cost in India,” May 2026

- a public finance research institute, “Indian Banks: Asset Quality & Profitability Analysis (NBFC GNPA at 3.4%),” January 2025

- an EV service guide, “EV Battery Life in India: Degradation, Warranty & Replacement Costs,” April 2026

- an automotive trade publication, “The 34% Surge: How NBFC Muscle Is Engineering India’s Used Car Financing Reset,” May 2026

- an energy research firm, “Lithium Ion Battery Pack Prices Fall to $108/kWh,” December 2025

- an industry trade body, “Electric Vehicle Industry in India: Growth, Trends & Policy,” 2026

- a market research firm, “India Electric Vehicle Market Size & Report 2034,” 2025

- a venture capital firm, “EV Financing: A Double Edged Sword for Early Stage Investing,” April 2025

- a business publication, “NBFC Vehicle Loan AUM to Grow 16–17% a Year; Reach ₹11 Trillion by FY27,” December 2025